Latest News

Newbridge Advises Transmission Capital Partners On Moray East OFTO

Transmission Capital Partners, a consortium comprising International Public Partnerships Ltd (“INPP”), Amber Infrastructure Group and Transmission Investment (the “Consortium”) successfully...

Newbridge advises Transmission Capital Partners on Moray East OFTO

Transmission Capital Partners, a consortium comprising International Public Partnerships Ltd (“INPP”), Amber Infrastructure Group and Transmission Investment (the “Consortium”) successfully reached financial close for the long-term ownership and operation of the Moray East Offshore Transmission assets (the “OFTO”) on 15 February.

The project will be the Consortium’s eleventh OFTO investment and relates to the transmission cable connection to the Moray East wind farm located approximately 22km off the coast of Scotland in the Moray Firth. The wind farm consists of 100 turbines that can produce 950MW of clean energy, enough to power over 1.4 million homes. The OFTO includes a 220kV 3-cable connection to the wind farm and the new onshore substation facilities at New Deer in Aberdeenshire.

Newbridge advised the Consortium on the raising of project level senior debt from a group of banks and institutions plus associated interest rate and inflation hedging.Newbridge – Review Of 2023

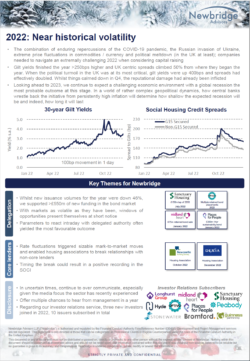

2023 has been a busy year across the infrastructure and development markets. On Development and Regeneration Newbridge has advised over...

Newbridge – Review of 2023

Newbridge Advises Transmission Capital Partners On East Anglia One OFTO

Transmission Capital Partners, a consortium comprising International Public Partnerships Ltd ("INPP"), Amber Infrastructure Group and Transmission Investment (the "Consortium"), successfully...

Newbridge advises Transmission Capital Partners on East Anglia One OFTO

Newbridge Advises Yorkshire Water On Large-scale Solar Procurement

The water sector in England has made a public commitment to be carbon net zero by 2030. Newbridge Advisors, as...

Newbridge advises Yorkshire Water on large-scale solar procurement

Sanctuary Taps Its 2.375% 2050 By £150m

Newbridge was delighted to have advised Sanctuary Group with the £150m tap of its 2.375% secured bonds due 2050. Sanctuary,...

Sanctuary taps its 2.375% 2050 by £150m

Carbon Credits & Offsetting

Download PDF If you would like to discuss carbon credits and offsetting in more detail, please contact the author of...

Carbon Credits & Offsetting

Download PDF

If you would like to discuss carbon credits and offsetting in more detail, please contact the author of this article Chris Evans - chris.evans@newbridge.co.uk, +44 7738 556 155.

Download PDF

If you would like to discuss carbon credits and offsetting in more detail, please contact the author of this article Chris Evans - chris.evans@newbridge.co.uk, +44 7738 556 155.

Sustainable Finance Framework

Newbridge is delighted to have advised Chelmer Housing Partnership (“CHP”) with the creation of its Sustainable Finance Framework. The framework represents...

Sustainable Finance Framework

Newbridge is delighted to have advised Chelmer Housing Partnership (“CHP”) with the creation of its Sustainable Finance Framework.

The framework represents an important tool for CHP in supporting it to achieve ambitious environmental and social targets. Future financing will play a key role in meeting these targets and the framework facilitates the formal connection to debt being linked to ESG.

It received external accreditation from Sustainalytics, which gives lenders as well as investors confidence that the framework aligns with industry standards.

Rich Wilsher, Head of Corporate Finance “I'm thrilled to issue our first Sustainable Finance Framework. Supported by Newbridge, we've set ourselves some bold and transparent ESG objectives, and I'm looking forward to working with our lenders and investors to bring these to life.“

Newbridge has supported a number of clients in establishing their frameworks, a prerequisite to labelling a listed debt instrument as green, social or sustainable. It also can be used for Private Placements as well as Term Loans and Revolving Credit Facilities.

Newbridge Supports Disasters Emergency Committee

Newbridge is proud to have donated to Disasters Emergency Committee (DEC) Ukraine Humanitarian Appeal to support those affected by the...

Newbridge supports Disasters Emergency Committee

Newbridge is proud to have donated to Disasters Emergency Committee (DEC) Ukraine Humanitarian Appeal to support those affected by the war in Ukraine.

If you'd also like to donate to the appeal, please click here.

Midland Heart Sells £75m Retained Bonds – 1.831% 2050

Newbridge acted as financial advisor for the sale of £75m retained bonds. The bonds were originally issued in August 2020....

Midland Heart sells £75m retained bonds – 1.831% 2050

Newbridge acted as financial advisor for the sale of £75m retained bonds. The bonds were originally issued in August 2020.

Joe Reeves, Executive Director of Finance and Growth, said: “We're delighted to have sold a further £75m of our £250m retained bonds in the capital markets. This money will be put to good use as we develop 4,000 high quality, affordable homes by 2025, modernise our retirement living offer and invest in the comfort and safety of our existing homes.”

Barclays acted as sole bookrunner, Newbridge as financial advisers and Trowers and Hamlin as legal advisers.“Public Private Partnerships: Driving Growth, Building Resilience” A Newbridge Practical Guide To Local Government PPPs

The Local Government Association commissioned Newbridge Advisors and PRD to produce a good practice guide on PPPs – Public Private Partnerships:...

“Public Private Partnerships: Driving Growth, Building Resilience” A Newbridge practical guide to Local Government PPPs

Longhurst Forward Sells A £100 Tap Of Its 3.250% 2043

Newbridge supported Longhurst Group forward place a tap of its 3.250% May-2043 across three settlement dates. The £100m tap, which...

Longhurst forward sells a £100 tap of its 3.250% 2043

Newbridge Advises Optivo On Their Retained Bond Sale

Optivo has successfully sold all of the remaining Retained Bonds of their 2035 bond issue, a nominal amount of £100...

Newbridge advises Optivo on their Retained Bond sale

Social Housing Mergers – Successes, Failures And Managing Stakeholders

Merger activity within the social housing sector has stepped up significantly over recent years and whilst many have been successful...

Social Housing Mergers – Successes, Failures and Managing Stakeholders

Archive

- 2024

- March

- January

- 2023

- January

- 2022

- December

- September

- August

- May

- April

- February

- January

- 2021

- September

- August

- June

- April

- March

- February

- 2020

- September

- July

- June

- May

- March

- 2019

- December

- July

- March

- February

- January

- 2018

- October

- September

- July

- June

- April

- February

- January

- 2017

- October

- July

- May

- March

- 2016

- December

- November

- September

- July

- June

- May

- March

- February

- 2015

- December

- April

- March

- February

- January

- 2014

- November

- October

- July

- February

- 2013

- November

- July

- April

- 2012

- November

- October